Report Summary.

Market Review: 2022 PVC market is mainly dominated by strong expectations and weak reality on the demand side:.

(1) In January, the policy side was boosted by strong expectations.

(2) In February, downstream demand was in the off-season, with a slow recovery in post-holiday starts.

(3) In March, crude oil rose sharply and domestic growth stabilization was expected to boost.

(4) April-May, the impact of the epidemic, domestic demand performance is sluggish.

(5) In early June, Shanghai was unsealed and the demand side was expected to rise again.

(6) in mid to late June, domestic demand still has not improved, the speed of accumulation of storage accelerated.

Raw material side: the first half of 2022 raw material side calcium carbide is difficult to provide cost support. The supply of calcium carbide is determined by its own start-up and PVC demand. just demand for PVC is unstable, dragging down the center of gravity of calcium carbide. By the impact of profit squeeze, this year’s calcium carbide start rate has declined compared to the same period last year, the supply side has been reduced.

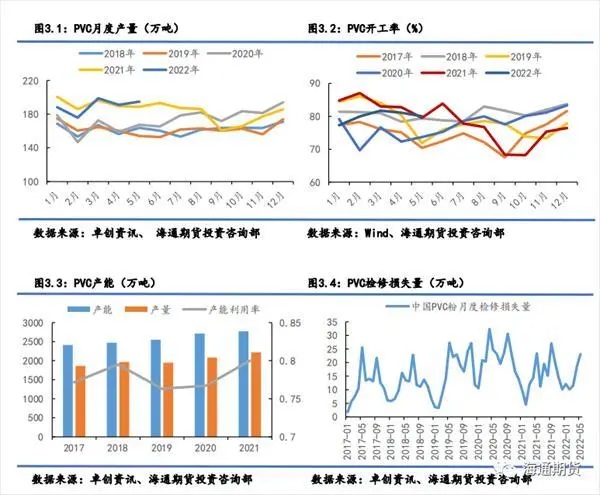

Supply side: PVC starts mainly consider their own profits, PVC producers in the first half of most of the time better profits, PVC starts this year is still at a historically high level. Subsequent to the subsequent reduction in maintenance, the supply side may increase smoothly.

Demand side: PVC is a post-cycle commodity of real estate, and the end demand is linked to real estate. In the second half of the year, PVC demand is expected to release limited space, while external demand may weaken, the demand side is expected to improve but the magnitude is limited. second half of 2022 we estimate that PVC supply and demand may be marginal improvement compared to the first half of the year, but the magnitude of improvement brought by demand is limited, PVC or oscillating weak trend, the market continues to speculate on the demand side of the “strong expectations “and “weak reality”.

I. Market Review

PVC market in 2022 is mainly dominated by strong expectations and weak reality on the demand side. We can divide the first half of the market into six stages.

(1) January, the central bank announced an interest rate cut, monetary policy easing is still room, and the market is optimistic about the first quarter infrastructure power, PVC in strong expectations of strong oscillation.

(2) February, weak reality dominated the movement of futures prices, downstream demand in the off-season, the slow recovery of post-holiday start-ups, PVC inventory pressure is high.

(3) March, overseas crude oil surge led to the collective upward movement of commodities, domestic growth is expected to boost exports and domestic demand recovery to support the rebound in PVC futures prices.

(5) In early June, with the unsealing of Shanghai, the demand side is expected to rise again.

(6) in mid-to-late June, the actual situation of domestic demand has not yet improved, external demand has turned weak, the speed of accumulation of storage accelerated, PVC futures prices broke down.

Second, raw materials: calcium carbide cost support is insufficient

The first half of 2022 raw material side of calcium carbide is difficult to provide cost support. Unlike 2021, this year, calcium carbide by the power limit disturbance weakened, calcium carbide supply by their own start and PVC demand decision. pvc just unstable demand, dragging down the center of gravity of calcium carbide decline, resulting in some calcium carbide companies have losses, shipping pressure increased, there are price cuts to make profits shipping behavior. Influenced by the profit squeeze, this year’s calcium carbide start rate has declined compared to the same period last year, the supply side has been reduced. The current PVC device overhaul more, resulting in a decline in demand for calcium carbide, calcium carbide profits under pressure, the start rate fell, with the subsequent reduction in PVC overhaul devices, calcium carbide demand is expected to increase, profits or repair, driving the supply back up.

The main cost of calcium carbide lies in the lan carbon, electricity and limestone. The supply and demand pattern of lancan is loose, without energy consumption double control and other disturbances, and the price follows the fluctuation of coal price more. While the demand pressure from downstream enterprises, lancan enterprises are also suffering from the cost pressure brought by the slow decline of raw material lump coal.

Third, the supply side: new production capacity is released slowly, and the start-up rate is affected by profits

The release of new PVC production capacity is slow. In recent years, PVC new production capacity is put into operation at a lower rate than expected, although there are more production plans, but the vast majority of them are planned to be put into operation this year and not implemented and moved back to the capacity, the actual production process is slow. PVC production is thus affected by the stock of devices. PVC starts mainly consider their own profits, in March due to better profits, some PVC companies postponed maintenance to May, March starts reached 81% beyond the average level of previous years. 2022 January-May total production reached 9.687 million tons, slightly lower than the level of 9.609 million tons in the same period last year, exceeding the average level of previous years. Overall, the rapid decline in the cost side of the price of calcium carbide, PVC producers most of the time better profits, so although the level of decline compared to the same period last year, this year the PVC start rate is still at a historically high level.

China’s reliance on imported PVC sources is not high, the scale of the import market is difficult to open, and the scale of imports this year is significantly lower than the level of previous years. Foreign devices are mainly ethylene-based process, so the price is high, imported sources of overall domestic supply will be more limited to enhance the role.

Fourth, the demand side: strong export support, domestic demand “strong expectations” lost to “weak reality”

The company’s main objective is to provide a strong and reliable service to its customers. The first quarter is the off-season demand, PVC consumption seasonal characteristics are obvious, showing a decline and then rebound trend. In the second quarter, with the temperature picking up, PVC gradually entered the peak season, but the performance of the demand side in April was less than the market expectations. In terms of external demand, PVC exports grew beyond expectations in the first half of the year, with a significant pull from foreign trade. 1.0189 million tons were exported from January to May, exceeding the same period last year by 4.8%. Domestic calcium carbide process has obvious price advantage compared to overseas ethylene process, and export arbitrage window opened. The expiration of India’s anti-dumping policy has increased the price advantage of China’s PVC powder exports, with explosive growth in exports in April and a single-month peak export volume.

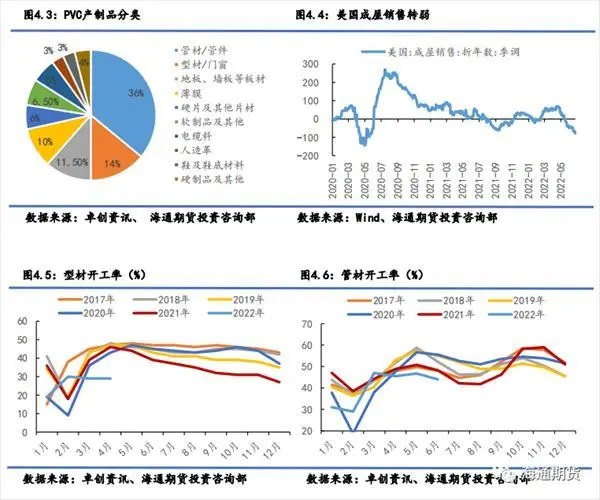

As overseas ushered in a tide of interest rate hikes, overseas economic growth will slow in the second half of the year, the lack of external demand will lead to PVC export growth is prone to a sharp drop, but net export volume is expected to continue to maintain. May U.S. second home equivalent annual rate sales fell 3.4 percent to 5.41 million units, the lowest level since June 2020, highlighting the inhibiting effect of high home prices and soaring mortgage rates on demand for housing. With the fall in U.S. real estate sales data, the demand for PVC flooring imports will weaken. pvc is widely used, downstream products are mainly divided into two categories of hard goods and soft products. Among them, pipes and fittings are the largest area of PVC consumption in China, accounting for about 36% of total PVC consumption; profiles, doors and windows are the second largest area of consumption, accounting for about 14% of total PVC consumption, mainly used to make doors and windows and energy-saving materials. In addition, PVC is also widely used in flooring, wall panels and other panels, films, hard sheets and other sheets, soft products and other fields. PVC pipes and profiles are mainly used in real estate and infrastructure and other fields, and consumption shows certain seasonal characteristics, with centralized stocking before and after the Spring Festival → peak consumption season in the second quarter → golden ninth and silver tenth → light at the end of the year. In the past two years is a year-on-year increasing trend, January-May PVC flooring total exports of 2.253 million tons, mainly exported to Europe and the United States developed countries.

Real estate investment continues to weaken, in addition to the completion of a single month growth rate did not continue downward, sales, new construction, construction, land acquisition growth rate continue to dip and the magnitude is large, until May the decline has narrowed. Policy has begun to force, adjusting the first suite mortgage rate floor, five-year LPR lower than expected and some cities gradually release the purchase and loan restrictions, intended to improve the need to stabilize expectations, the real estate market is expected to zigzag repair later.

PVC is a post-cycle commodity of real estate, the end demand is linked to real estate, real estate demand for PVC lags. PVC apparent consumption has a high correlation with completion, slightly behind new construction. downstream product factory start-up in March gradually increased, into the second quarter belongs to the peak demand season, but the actual performance is less than market expectations. Due to the repeated impact of the epidemic on the order quantity, the start-up rate of downstream enterprises in April and May was far below the level of previous years. The release of actual demand needs time process, PVC just follow up still need to wait.

V. Inventory: high inventory pressure

PVC social inventory seasonal pattern: first quarter accumulation → second quarter decline → three quarter continued to depot → fourth quarter replenishment. 1-3 months in the off-season consumption, PVC seasonal accumulation to the average level in previous years. However, the slow pace of de-stocking in March-May was mainly due to weak domestic demand, relying on strong external demand to barely de-stocking. From mid-to-late May, PVC external demand turned slightly weaker, and domestic demand remained weak, leading to the beginning of PVC accumulation.

VI. Outlook for the second half of 2022: limited improvement in domestic demand, the price pivot down

According to the coal price of 800 yuan / ton, the cost of lanthan 1250 yuan / ton, 100 yuan / ton profit, electricity prices do not float 0.25 yuan, corresponding to the cost of calcium carbide about 3000 yuan / ton, according to the average profit level of 400 yuan / ton of calcium carbide, calcium carbide price 3400 yuan / ton, freight 400 yuan / ton, external extraction of calcium carbide price at 3800 yuan / ton, corresponding to the cost of PVC East China 6800 yuan / ton, profit -500 to +1500 fluctuations, the measured price of PVC in 6300-8300 oscillation.

Raw material side: the first half of 2022 raw material side calcium carbide is difficult to provide cost support. Unlike 2021, this year, calcium carbide by the power limit perturbation weakened, calcium carbide supply by their own start and PVC demand decision. pvc just unstable demand, dragging down the center of gravity of calcium carbide decline, resulting in some calcium carbide companies have losses, shipping pressure increased, there are price cuts to give profit shipping behavior. Influenced by the profit squeeze, this year’s calcium carbide start rate has declined compared to the same period last year, the supply side has been reduced.

Supply side: PVC start rate mainly considering their own profits, PVC producers in the first half of most of the time better profits, so although the level of decline compared to the same period last year, PVC start rate this year is still at a historically high level. Subsequent to the reduction in subsequent maintenance, the supply side of PVC may be under pressure.

The PVC consumption is highly correlated with completion and slightly lags behind new construction. 2022 domestic interest rate cuts overlaid with growth stabilization initiatives, the demand side has repeatedly appeared strong expectations, despite the expected growth in exports, but domestic demand has not been able to recover significantly, weak reality over strong expectations. The second half of the slow recovery of real estate, PVC demand is expected to release limited space, while external demand may weaken, a comprehensive view, the demand side is expected to improve but the magnitude is limited.

In the second half of 2022, we estimate that PVC supply and demand may show marginal improvement compared to the first half of the year, but the demand will bring limited improvement, PVC price center of gravity may be oscillating weak trend, PVC is expected to fluctuate in the range of 6300-8300, the market or continue to speculate on the demand side of the “strong expectations” and “weak reality”. (Source: Haitong Futures, if there is infringement contact deleted)